The reality of life in the United State is such that your creditworthiness means the difference between making ends meet and living a good life. It is incredibly hard to live in the US exclusively by the cash in hand. Most of us have to get a line of credit at some point in our lives – be it a car or a house purchase. If we are not prepared, this can be a costly endeavor. In this post, we will go over some basics of credit score calculation and how to build good credit history quickly.

How credit works

The idea behind credit is that the borrower of credit (you) obtains instant access to a lump sum of money upfront and agrees to repay that amount back to the lender (the bank) over a period of time and under conditions of that credit agreement. Two most important parameters of the credit are:

- Payback period – an amount of time between getting access to the lump sum of money and the time the last payment on that credit is made by the borrower.

- Annual Percent Rate (the so-called APR) which defines how much money a lender will charge on the outstanding balance on the credit. It is calculated as a percent of that balance, hence the name APR.

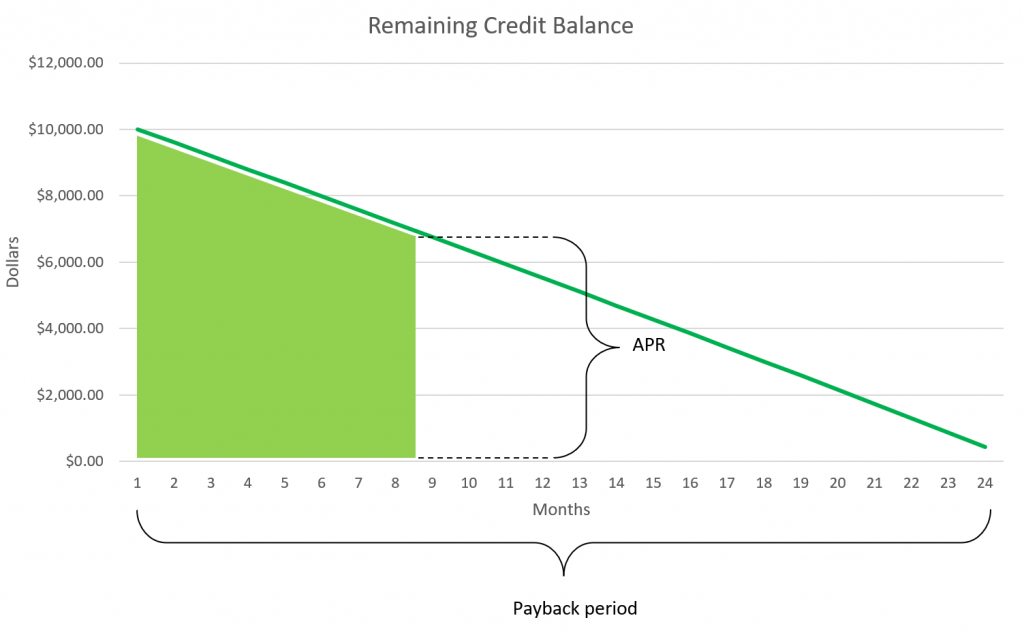

For example, for a 2 year credit for $10,000, APR is calculated on remaining balance as shown on the picture below.

The third parameter which lenders put less emphasis on, yet it is equally important for the full picture – compounding period. APR designates an annual percentage rate, but lenders can compound interest monthly, or even, bi-weekly. In this case, a monthly periodic rate is applied at the end of every month. For example, if APR is 5% and the compounding period is 1 month, then every month lender will assess 0.05 / 12 = 0.00416 interest rate on the remaining balance.

How much an APR impacts your wallet

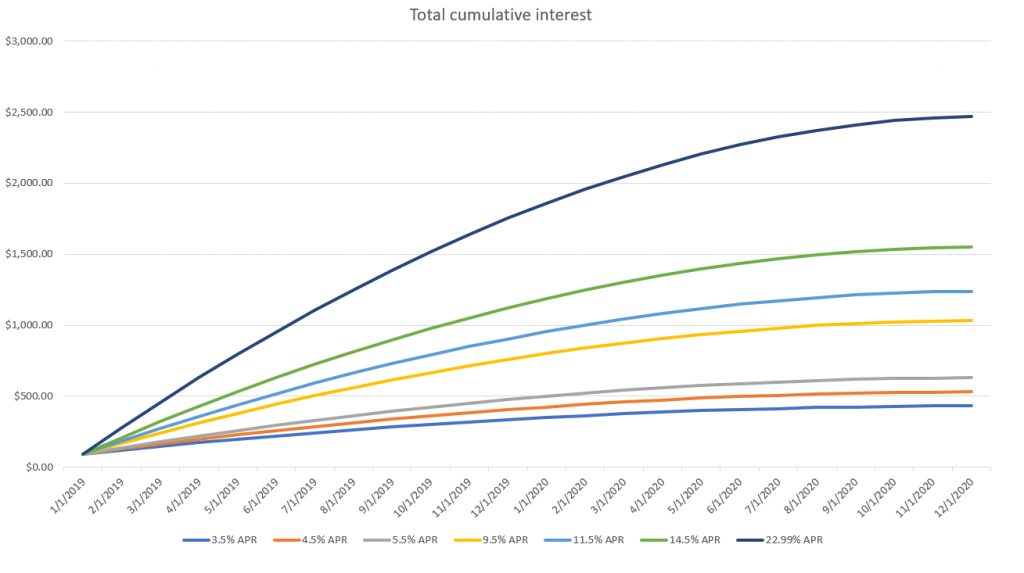

It is obvious that the higher the interest rate the more it costs you to use the credit. You may also notice that as you pay a part of your credit every month, the dollar amount of interest charged on remaining balance decreases. If we look at various interest rates for $10,000 credit over 2 years and add all interest paid every month the difference would be drastic.

Total interest paid on 3.5% APR would $432.82. At the same time, 22.99% APR would cost $2,470.14. 22.99% APR is very real for a lot of Americans who do not pay their credit card debt in full every month.

Fixed vs. variable APR

The simplest form of APR is the one that stays the same, no matter the market conditions. Fixed APR are spelled out explicitly in credit agreements and lender cannot change them, unless a new agreement is signed.

Variable APR can change over time of credit because it is tied to an index or a rate at which Federal Reserve lends money to other banks. When economy is doing great, rates tend to up and so your APR will go up. As economy takes downturn, Federal Reserve will likely lower the rates and so will your APR go down.

To make matters more complicated, there are Adjustable Rate Mortgages. They are defined by two numbers – X/Y, where X means the duration of time the rate is fixed and Y indicating the frequency at which the rate is recalculated after initial period of X years passes.

Monthly vs. bi-weekly payment

It doesn’t help to pay credit more frequently than compounding period because all of the payments made between two compounding periods will be lumped together into a single payment from interest point of view. However, there is a difference between paying monthly and bi-weekly.

There are 12 months in a year so making payments monthly produces exactly 12 payments a year. On the other hand, there are 52 weeks a year, which means there will be 26 bi-weekly payments a year. Comparing to making two payments a month, which produce 24 payments a year, bi-weekly payments make 2 extra payments. It is as-if you made 13 monthly payments a year. That’s the trick that makes bi-weekly payments look “faster” than monthly.

Credit score

One of the most important numbers impacting which interest rate you qualify for is your FICO credit score. This score is calculated by 3 credit bureaus – Equifax, TransUnion and Experian using an algorithm that FICO invented. myFico explains how the score is calculated the best.

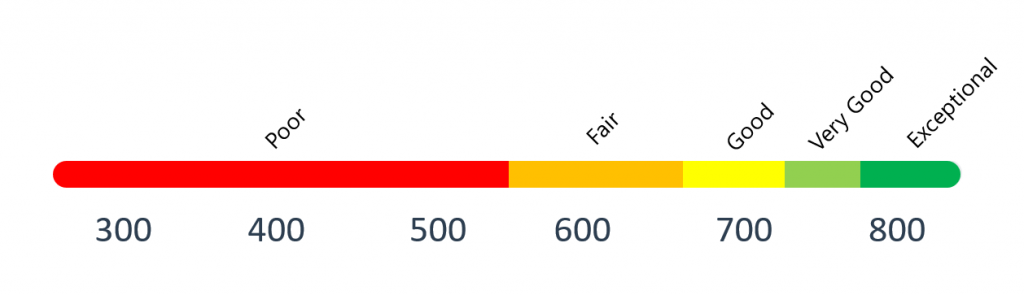

Generally speaking, the FICO score is a number between 280 and 850, assigned to every individual that has a credit history. If you do not have a credit history, your score is not zero, but rather, it doesn’t exist. Interesting fact, roughly 26 million Americans do not have a credit score.

Credit scores are calculated only when a credit report is pulled from one of the bureaus. There is no historical credit history trend that is calculated for every individual. As such you can’t go back in time and request your credit score as of 2 years ago. However, if you have an account with one of the credit bureaus and you pull your credit report periodically, your credit score history will be stored in your profile.

When you start building credit history you don’t start with 280 and go up from there. 280 credit score indicates damages to your credit profile. It usually takes at least 3 months for your credit history to start flowing to credit bureaus from your lenders. The FICO scoring model requires at least 6 months of history to generate a number. If you haven’t done anything horribly bad and you were paying your bills on time, your starting score will be in Good or Very Good range.

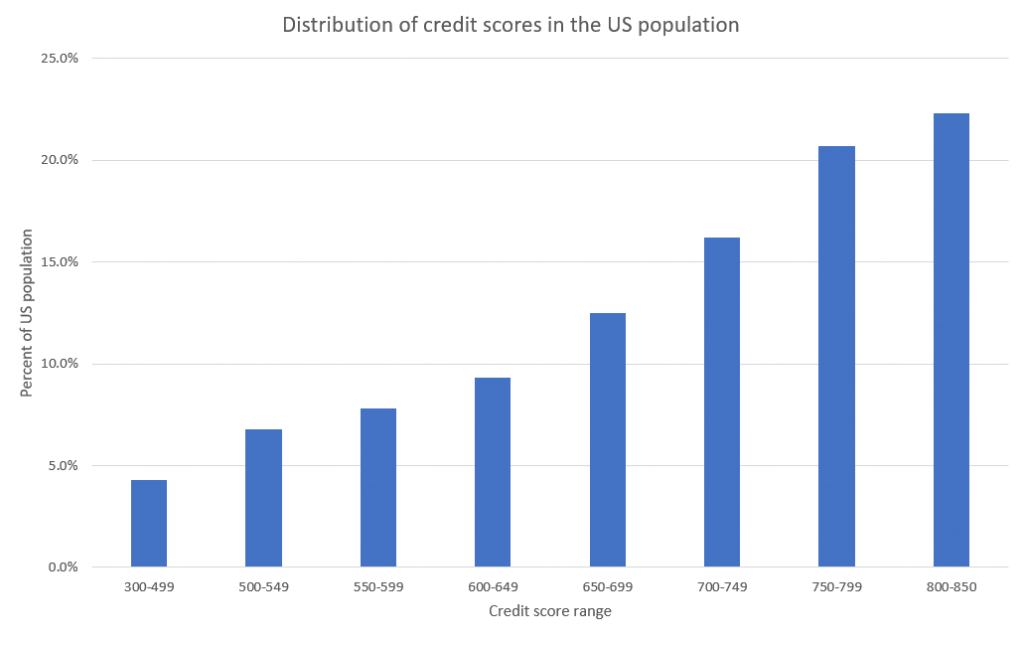

According to fico.com, distribution of credit scores in the US population looks as indicated below. About 43% of people who have a credit score, have a very good one or exception.

Creditworthiness

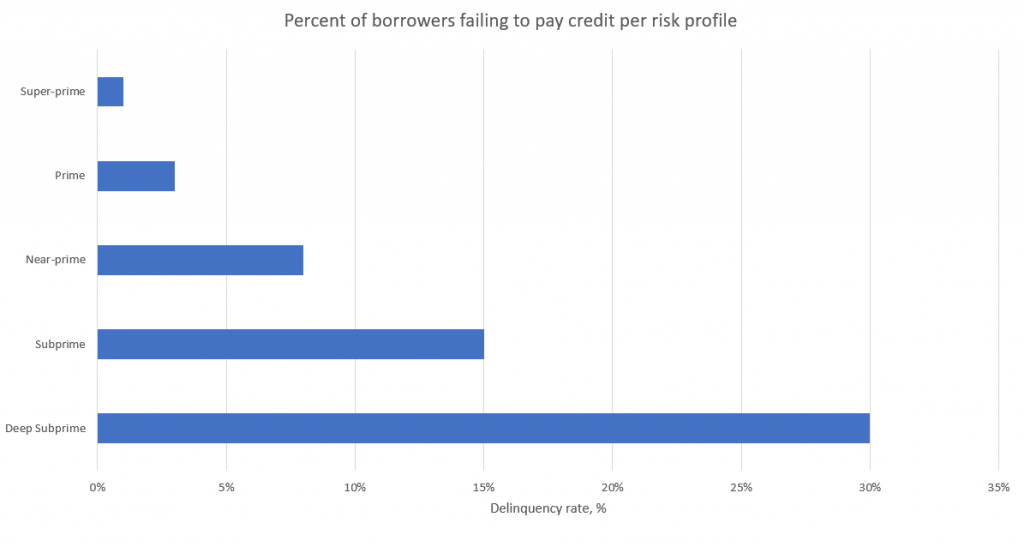

Even though every individual is evaluated personally when applying for a line of credit, consumer finance bureau classifies borrowers into buckets based on broad risk profile:

- Deep subprime – credit scores below 580

- Subprime – credit scores of 580 – 619

- Near-prime – credit scores of 620 – 659

- Prime – credit scores of 660 – 719

- Super-prime – credit scores of 720 or above

These risk profiles have vastly different delinquency rates, which influence the interest rates at which people get credit. The higher the risk of a borrower going bankrupt, the higher is the interest rate at which that borrower is approved for credit. If you have a low credit score it means you have been unable to keep your promise to the lender in the past and future lenders don’t like that.

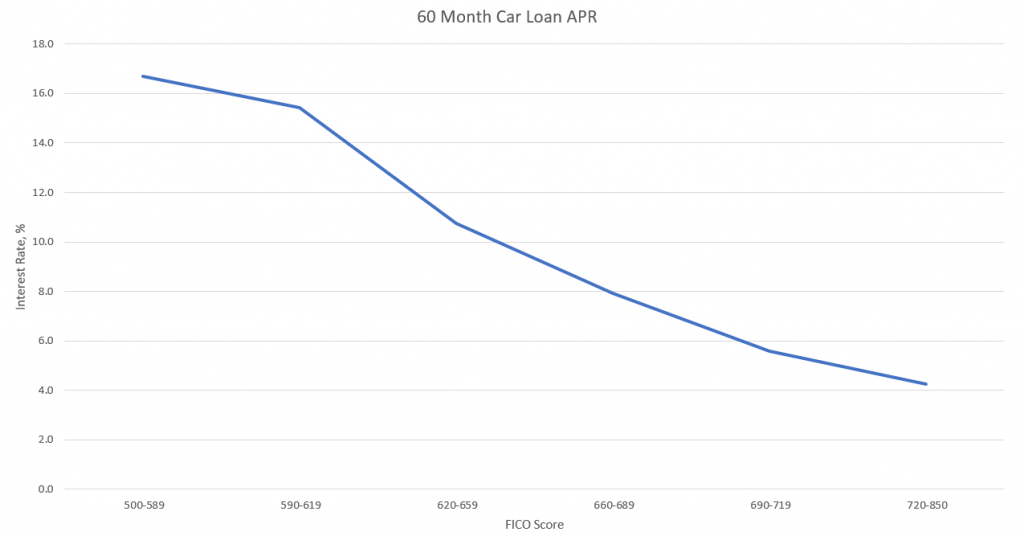

As the credit score increases, the credit interest rate drops, according to fico.com. Having excellent credit history and being a super-prime borrower really means the world of difference. You go from making ends meet on one end to living a comfortable life without financial stress on the other end of the FICO score spectrum.

Types of credit

Your credit score depends on variety of lines of credit you have so we should talk about them.

- Installment – this is a type of credit that is issued for a fixed sum of money and you just have to pay it back over a period of time. When the outstanding balance reaches $0 this credit terminates. A car loan or mortgage would be two examples of such credit.

- Revolving – you are allowed to borrow up to a certain amount of money and you have to repay what you have borrowed only, not the entire line of credit. When the outstanding balance reaches $0 this line of credit stays open until you choose to close it. A typical example of such credit is a credit card.

- Service credit – you are obtaining services from various companies and you have to pay for them at the end of the billing cycle. Utilities, gym membership, cell phone service, internet are all examples of service credit.

For completeness, we should mention that there are charge credit cards as well. You have to pay them in full every month and cannot carry a balance. They are not classified as revolving because there is no revolving debt on them.

| Credit | Type | APR | What is it for? |

|---|---|---|---|

| Mortgage | Installment | 3.5% – 6% | It is very common for people to mortgage a house. This is a closed-ended loan when the bank obtains a lien to your property and holds it until you pay it off completely. Typically mortgages are secured for 15 or 30 years. |

| Car Loan | Installment | 3% – 15% | 44% of Americans use loans to buy cars. Typically these loans are for 60 months and carry a fixed rate. |

| Appliance Loan | Installment | 5% – 20% | These loans are used to buy major appliances at the stores (like a fridge) and are usually financed by the store itself. When stores are motivated to sell, they can give these loans at 0% APR for super-prime borrowers. |

| Payday Loan | Installment | 300% – 600% | These are the worst type of loans you can imagine. They are supposed to help people make ends meet between two paychecks, but in reality, they send people into deeper debt. They carry high interest rates and must be paid in 2 weeks. |

| Personal Loans | Installment | 5% – 12% | Financial institutions can issue unsecured personal loans to individuals for whatever people may want to do. These loans are typically in $10,000 – $40,000 range and carry lower APR than the credit card. |

| Student Loan | Installment | 4.5% – 8% | People get this loan to cover their education costs, which are pretty high in the US. The catch with these loans is that they are not forgiven even in bankruptcy. You will carry this loan until either you pay it off or you die. The upside, is you have to pay a portion of your income into the loan, so when you lose your job and lose income, you don’t have to pay. |

| Credit card | Revolving | 25% – 29% | This is a prime tool for building credit history but it is a very sharp knife if you decide to carry a balance. Credit cards have insanely high APR. It is best to pay them in full every month. You do “cash advances” on your credit card up to a few hundred dollars and payback at even higher APR. |

| HELOC | Revolving | 3.15% – 6% | HELOC stands for Home Equity Line of Credit. You can take part of your house and get a line of credit for it. The risk is obvious – if you fail to repay this credit as agreed, you can lose your house. However, if you need money quickly and income is not a problem – you can get HELOC to do renovations in your house. |

How credit affects your life

Your creditworthiness affects your life beyond financial side. More and more businesses and government agencies start relying on credit history and score to make decisions.

- Your employer will most likely conduct a background check to make sure you do not have negative public records and you can be trusted to perform job responsibilities

- Your landlord will definitely run a credit score check when you apply. Landlords want to make sure you will pay rent on time and will not trash their property. Your credit score is a big factor in the decision to let you rent a property.

- Cell phone and internet companies will pull your credit report to make sure you will pay your bills on time before activating your account.

- Your insurance rates depend on your credit score.

- It is becoming more common among adults to ask for a credit score of each other to decide whether to continue dating. This is driven by all factors above. Individuals with poor credit scores and high outstanding debt can negatively impact family life down the road.

- Certain businesses and government agencies are using credit history to confirm people’s identities. They ask questions like “did you live at this address?” or “who do you have a credit card with?” and match your responses to information in your credit profile.

Factors that affect your credit

Experian has a comprehensive article about issues affecting your credit score. I suggest taking a quick detour and reading that post. In the remainder of this section, I will cover factors that I have experienced personally.

Length of credit history

The number one thing that affects new immigrants is the length of history. Even after over a decade of living in the US, this is the biggest drag on my credit score. You need to have at least 7 years of credit history to be a candidate for super-prime borrower status. Credit bureaus look at all your credit accounts, calculate an average age among them and want to see it be over 7 years. This is hard to achieve for someone who just moved to the US.

The consequence of this factor is that you want to keep your oldest credit card account active, even if you do not use it anymore. It helps increase the average length of credit and therefore pushes you into higher credit scores.

Credit mix

The FICO score considers how many types of credit you have. They want to see at least 2 instances of each type of credit – installment and revolving. It is pretty easy to get 2 credit cards to satisfy revolving credit requirement. However to have 2 installments, you may need to get a mortgage. This is not something new immigrants should do until they really plant their roots.

Amount of new credit

You are rewarded for opening new credit cards and shopping for lower interest rates on your existing loans. However, if you do that too frequently then you suffer high number of inquiries on your credit profile, which drags your score down. As you add new lines of credit to your account you decrease the average length of credit history. So, if you catch my drift, you have to really want to go after this aspect to fine-tune the frequency of new applications perfectly.

How to build credit history right

Do not rush. Solid credit history takes time. It will be about 6 months before you see any fruits of your efforts. Strap in and prepare for a journey.

You might be tempted to apply for any credit card that lenders will give you. Don’t. It is counterproductive for your long term financial health. There are lenders out there that will underwrite people with poor credit. You don’t want to be associated with them, nor you want them to have your social security number. If your social security number leaks or is compromised you will be in some serious identity protection pain. Social Security Administration will change your number if you are a victim of identity theft. You will have to update the rest of the government bureaus and businesses, some are not prepared for an SSN change. Why ask for trouble?

Another reason to be picky with your lender is that you want to keep your oldest credit card, basically, forever. This will be the card that positively impacts the length of your credit history, which in turn increases your credit score. If you pick some garbage for the first card and then close it 2 years down the road, you will have wasted 2 years of credit history.

Strategy

Building a good credit history is an iterative process. During every iteration, you shoot high and take what you get. Solidify your standing with consistent payment history. Pull your credit report, analyze where you stand, take hints from credit bureaus. Rinse and repeat. The idea is to climb the credit score ladder higher every time you apply.

Being denied credit is useful

Start by applying to the credit card of your dreams or asking for a loan. Without credit history, you will likely get denied and in rejection letter lender will explain why. This information is valuable.

You should pack all your line of credit applications within 30 days. Every time you apply you take a hard inquiry on your credit report which lowers your score. However, credit bureaus will collapse all hard inquiries into a single one if they are all complete in about 45 days. So go ahead and apply to as many cards as make sense to you.

If you are denied, this information is not stored anywhere in the system and will not be used against you in the future. You can turn-around and re-apply again if you believe you qualify within a month. The lender will pull your new credit report and will re-run underwriting.

Shoot for the moon, get to the sky

If you like a particular credit card – go ahead and apply for it, within reason, of course. If you are a student with no credit history, American Express Platinum with a $550 annual membership fee is not reasonable. You can ask for a lower credit limit on the card, even if they cap you at $1,000 that’s irrelevant. If you plan to pay the card in full every month (which you absolutely should), ask for a higher APR if your credit score is low, to qualify. If you strongly believe you are close to landing a card, go ahead and call the lender customer service and try negotiating with them.

The same idea applies to all aspects of credit, not only credit card. If you want to rent an apartment and your credit score is low (or missing), call the landlord and negotiate. Want a better internet plan – go ahead and apply, be prepared to negotiate.

Know your number

You should be the first person that pulls your credit report. Get yourself an account with Equifax, TransUnion or Experian and watch your profile like a hawk. The credit bureau will give you tips on how to improve your score. For example, the Equifax credit report contains items that negatively impact your score. If you see things that don’t make sense – dispute them. Equifax personal account will cost you $19/month but you get unlimited credit profile requests.

Remember, you are entitled to a free credit report from each credit bureau once a year. The cheap and painful process is to send a regular USPS mail to each one asking to print your report and mail it back. A quicker but more expensive option – use your membership with the bureau to obtain electronic credit report from all three of them.

Experian offers credit score boost service. It may not be a bad idea to give it a shot, especially if you have no credit history at all.

Pay on time

All financial institutions publish your credit account information to credit bureaus in bulk every month. They send information such as credit limit, outstanding balance, payment history, APR, etc. Your billing cycle may not align with the date of publication so you will likely carry some balance during every upload. That’s not a big deal, just something to keep in mind.

It is absolutely critical to pay your bills before or on the due date. If you miss a payment by 1 day, just because the transaction posted one day later, and you have just damaged your credit score. It is not worth it. I recommend paying your bills on the day when they arrive. Do not wait for the last moment. If you automate your payments – it would be even better. Do not rely on yourself to keep making payments month after month – let computers deal with it.

Diversify

Lenders like to see you with multiple credit cards and lines of credit that are all paid on time. Get at least 2 credit cards, get a car loan or a mortgage. Do not do it all at the same time, but rather over time as you build your score and qualify for better rates. In absolute terms, car loans are not the best idea because you are paying interest on rapidly depreciating assets. However, for building your credit history, car loans are a cheap and easy trick.

An interesting chicken-and-egg problem is mortgage. You are unlikely to reach 800+ score without a mortgage so you need a mortgage to get there. Once you get there, you will qualify for better mortgage rates. So the plan is to get a mortgage, grow your score, then re-finance for better rates once you become a super-prime borrower.