A friend of mine who lives in Europe has gotten a job offer from a US employer. He reached out asking to help him decide whether relocation would be worth the trouble. His question made me realize how different compensation packages and taxation laws are between the EU and the US. It is hard to give a blanket answer on whether he should move to the US without breaking down the cost of living first.

US as a country is a great place economically, socially, geographically, politically, etc. Every year a lot of people make a decision to leave their home and move here in hopes of a better life. When money is not the question, then relocation to the US is a definitive yes. You can fulfill yourself as a photographer, be a tough journalist without fear of persecution, space engineer building rockets and first Mars colony, and so on. However, when money is one the reasons someone is considering the US, it warrants taking a moment to break down expenses. In absolute value, US salaries are vary attractive, especially considering they are quoted in annual income before taxes. Expenses, however, are very high as well and they very state by state, location by location. On top of that, tax code is convoluted and takes explanation from different angles to grok. Do not take this article as a professional tax advise because I am not a CPA. This article intended to paint a watermark for what you can expect to keep out of your earnings, which will help you decide whether US job is really that great.

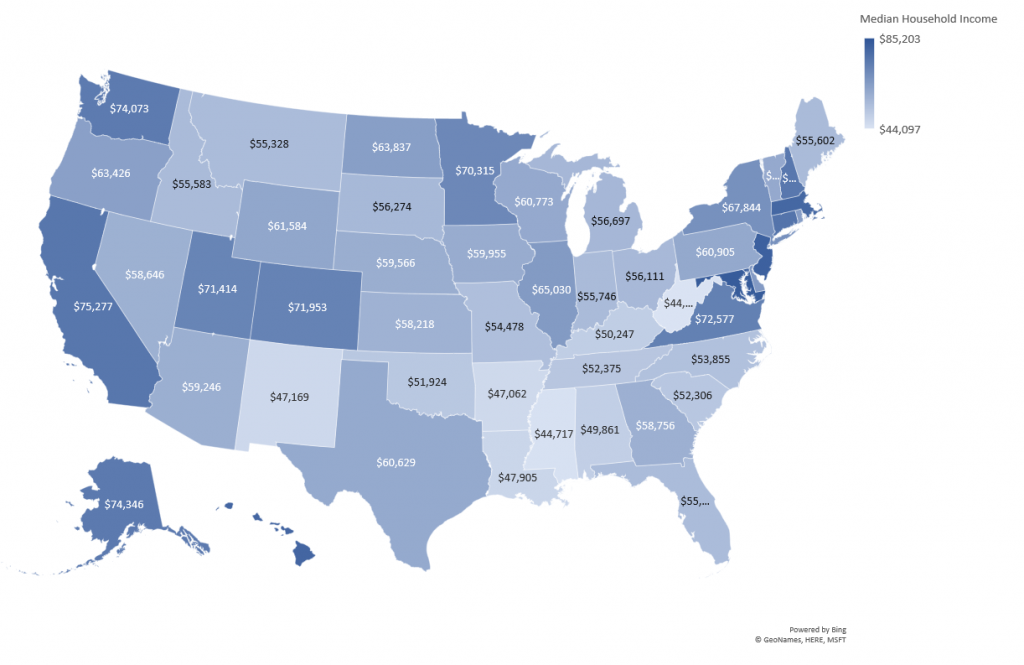

Income by State

Different states in US have different cost of living and, consequently, different income. The same exact job done in different states will be compensated differently.

General pattern is such that east and west cost are the most expensive to live and have highest incomes. Central and mid-western part of the United States have lower income and lower cost of living. The lowest income and cost of living is in the south. Use glassdoor.com or ziprecruiter.com to clarify your job compensation in different states.

Federal taxes

One of the biggest drags on your income is IRS, which stands for Internal Revenue Service. Your employer is required to withhold Federal taxes out of every paycheck and give you whatever remains. Your employer will ask you to fill form W4 when you start and he will automatically deduct your elected amount from the paycheck. Federal taxes are mostly comprised of the following 3 categories:

- Federal tax – progressive, based on income in the table below, for each bracket.

- Social Security (FICA) – 6.2% of your income, up to $137,700.00

- Medicare tax – 1.72%

Federal tax is calculated for each income bucket separately.

| Tax Rate | You are filing taxes by yourself | You are filing taxes with your spouse |

| 10% | $0 – $9,875 | $0 – $19,750 |

| 12% | $9,876 – $40,125 | $19,751 – $80,250 |

| 22% | $40,126 – $85,525 | $80,251 – $171,050 |

| 24% | $85,526 – $163,300 | $171,051 – $326,600 |

| 32% | $163,301 – $207,350 | $326,600 – $414,700 |

| 35% | $207,351 – $518,400 | $414,700 – $622,050 |

| 37% | over $518,401 | over $622,050 |

For example, if you are making $50,000 a year and you are filing yourself, you would calculate your federal tax as follows:

| Tax Rate | Income bucket | Your tax for the bucket |

| 10% | $0 – $9,875 | $9,875 x 10% = $987.50 |

| 12% | $9,876 – $40,125 | ($40,125 – $9,875) x 12% = $3,629.88 |

| 22% | $40,125 – $50,000 | ($50,000 – $40,125) x 22% = $2,172.50 |

So your federal tax will be $987.50 + $3,629.88 + $2,172.50 = $6,789.88, which is 13.57% of your annual income.

To reduce federal tax, IRS provides standard deduction for everyone. You can choose to itemize your deduction, if you have a complex tax situation, or you can claim standard deduction available for everyone. As a rule of thumb, it is not worth doing itemized deduction, unless you have mortgage, paid state income tax previous year, have a rental property, extensive medical bills, large tuition or business expenses. Since this article is catered towards people just starting their lives in the US, they are likely to stick to standard deduction.

The way standard deduction works is by “reducing your taxable income”, before calculating federal taxes. Standard deduction is substracted from annual income, and whatever remains, will have federal taxes assessed against it. For 2020 standard deduction has the following amounts:

| Your are filing taxes only for yourself | $12,400 |

| You are filing taxes with your spose together | $24,800 |

Now if we apply standard deduction to our example of $50,000 annual income above for individual filing on his own, we would have to assess taxes on $50,000 – $12,400 = $37,600 only.

A great way to reduce your federal taxes and take home more cash is to throw additional pre-tax deductions. Coverage of these deductions is out of scope of this post, but I will list them for completeness:

- 401(k) – this is your retirement contribution. Essentially government allows each individual to put up to $19,000 every year in tax-free dollars into a special investment account. This has to be sponsored by your employer. More details here. Exact limits can be found on IRS web site.

- IRA – if you can’t do 401(k), you may be able to open IRA, with similar benefits except employer match.

- HSA – stands for Health Savings Account. If you have a High Deductible Health Plan you may qualify to open a HSA and put money into it tax-free.

State taxes

Generally speaking, all US states collect taxes, one way or another. Some states have income tax, some have sales tax, and some collect both. Income tax is paid on the money you earn. Sales tax is assessed on the money you spend in the state. Out of 50 states, only the following states do not have state income tax, which they compensate with sales tax (sources are Kiplinger and Wikipedia):

- Alaska – no income or state sales tax, but local cities apply up to 7.5% sales tax

- Florida – on average 7.05% sales tax

- Nevada – 8.14% sales tax

- New Hampshire – no sales tax

- South Dakota – 6.4% average combined sales tax

- Tennessee – 9.47%

- Texas – 8.19%

- Washington – 9.21%. You can look-up specific tax rate here.

- Wyoming – 5.32%

The rest have a tax on income that needs to be paid on top of all federal taxes:

- Alabama – up to 6%

- Arizona – 2.8% – 4.54%

- Arkansas – up to 7%

- California – up to 13%

- Colorado – flat 4.63%

- Connecticut – 5% – 6.3%

- Delaware – 5% – 7%

- Georgia – 6%

- Hawaii – 8.25%

- Idaho – 7.4%

- Illinois – 4.95% of federal tax

- Indiana – 3.3% of federal tax

- Iowa – up to 8.98%

- Kansas – 4.6%

- Kentucky – up to 6.6%

- Louisiana – up to 6%

- Maine – 7.15%

- Maryland – 5% – 5.75%

- Massachusetts – 5.1%

- Michigan – 4.25%

- Minnesota – 5.35% – 9.85%

- Mississippi – 5%

- Missouri– 6%

- Montana – 6.9%

- Nebraska – 6.84%

- New Jersey – 3.5% – 8.97%

- New Mexico – 4.9%

- New York – 6.65% – 6.85%

- North Carolina – 5.75%

- North Dakota – 2.04% – 2.9%

- Ohio – up to 5%

- Oklahoma – 5%

- Oregon – 9.9%

- Pennsylvania – 3.07%

- Rhode Island – 4.75% – 5.99%

- South Carolina – 7%

- Utah – 5%

- Vermont – 6.8% -8.95%

- Virginia – 5.75%

- West Virginia – up to 6.5%

- Wisconsin – 6.27% – 7.65%

- D.C – 6% – 8.75%

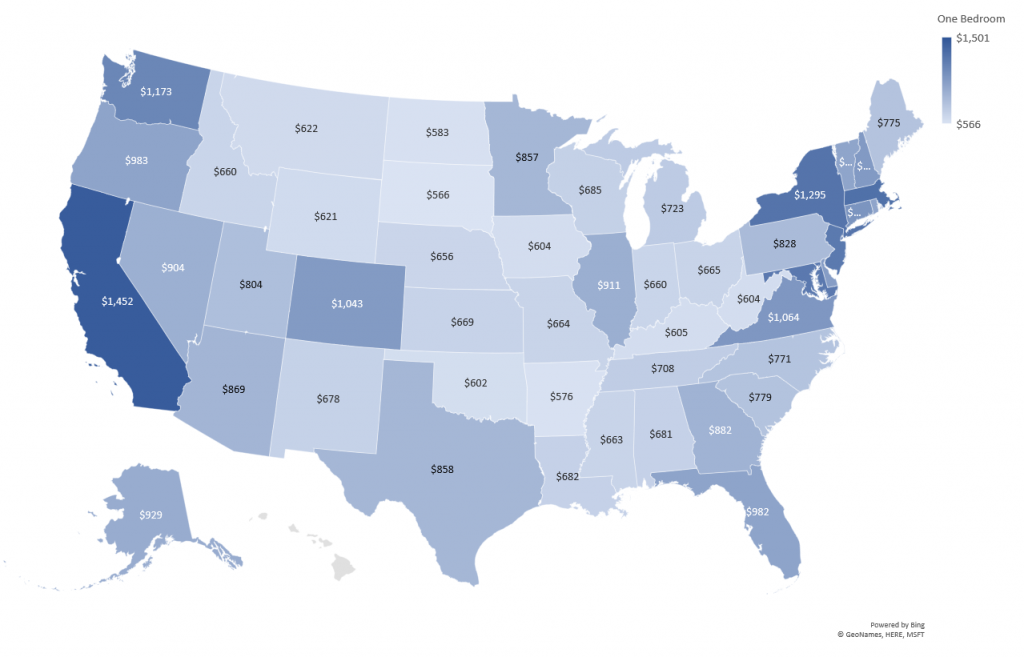

Housing

A big part of monthly expenses is rent or mortgage because you have to have a roof over your head. Let’s look at median state rent data for single bedroom apartment (source apartmentlist.com)

A single bedroom unit typically will have a kitchen and a common living area, bathroom, small closet and perhaps storage space, may come with laundry room as well. Usually single bedroom apartments are around 800 square feet in size, which is about 75 square meters.

Prices above are not reflective of individual metropolitan areas. For example, it is not possible to rent a single bedroom unit in Greater Seattle area for $1,173. Typical prices start north of $2,000. So if you are moving into a metropolitain area, please apply 2x multiplier to median prices on the map. Good resources to clarify exactly how much to expect to pay for a rental unit are zillow.com and apartments.com. For completeness, I should mention that you can also rent apartments on Craigslist, which will be cheaper but you run a risk of scam.

Rent is not tax-deductible and will have to be paid from the money remaining after all federal and state taxes are paid.

As a tenant, you must carry renter insurance to protect everything within the property. It covers your belongings, so-called “walls-in”. Typical run rate is about $20/month.

Buying a house

If you are an adventurous individual and would like to buy your own property as soon as you arrive into the US, I will break-down the math. However, I strongly advise against this path because it is incredibly risky and expensive. As a new resident, you will not have credit history with US credit bureaus and mortgage lenders will offer you money at exuberant rates. Typical mortgage rates for individuals with good credit are around 3.6% – 4.8% rate. Without credit history, you may be required to either put more money down, or get a loan at 8% APR, which is a complete rip-off.

In terms of risk, if you lose your job and you’re unable to keep monthly payments, bank will foreclose on your property and sell it. You will be left with nothing, even though you paid part of the mortgage principal down. In some cases, bank may take you to court and force to sell your belongings to repay part of the mortgage, which you may be able to avoid by filing for bankruptcy. You may also need a lawyer to file and those guys aren’t cheap.

If you are still determined to move forward with a house purchase after stern warning, check out current rates here. Interest rates are applied towards remaining balance on the mortgage. If you bought a house for $100,000 and paid $20,000 in principal – you owe $80,000 to the bank. Your mortgage interest is applied to these $80,000 and broken down monthly. In practice, the math is more complicated but we’re here to do ballpark, so at 4% APR on $80,000 principal you would awe $80,000 x 4% / 12 = $266 per month.

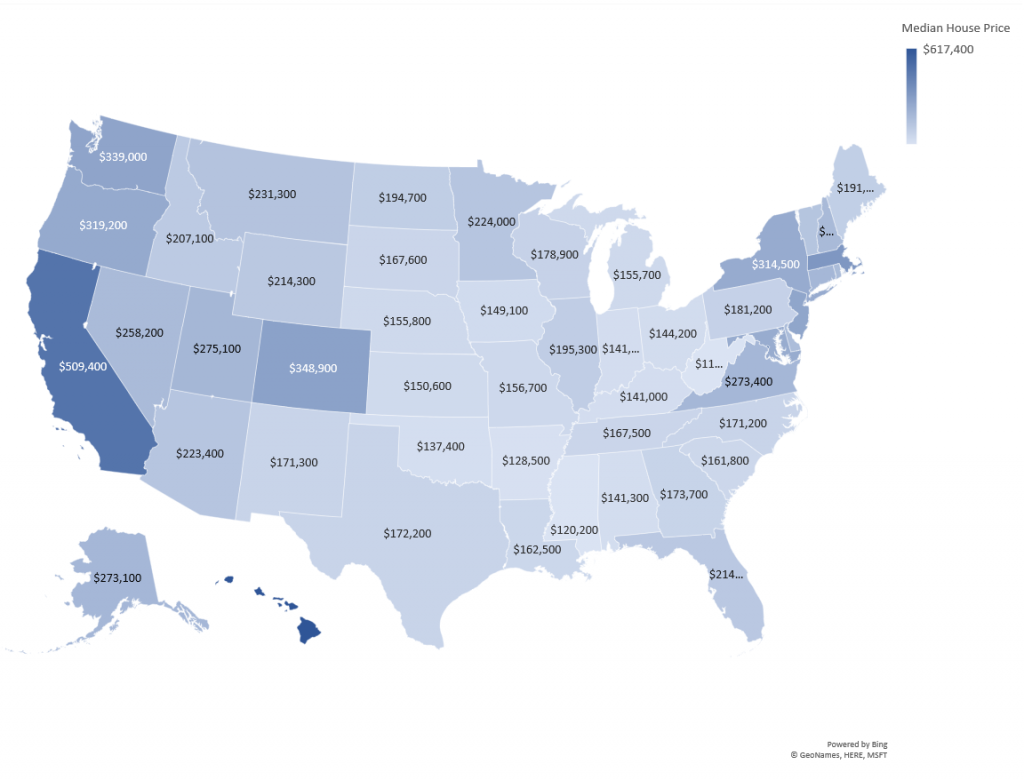

In reality, there are no $100,000 houses in the US. Let’s look at median house prices in every state (source CNBC):

Similar to median rental prices, these prices need to be multiplied by 2x if we are talking about metropolitain areas in each state. These prices may be representative of the house prices beyond 30 mile radius of the densely populated areas in each state.

Lenders usually require 20% down payment on the house to get a good rate and eliminate PMI – monthly mortgage insurance payment that is assessed until mortgage principal balance reaches 20% of the house value. Using a simple mortgage calculator, homeowner in Washington state who puts 20% down and applies 30 year fixed mortgage will be paying $1,597.25 on median-priced home. A resident of Greater Seattle area will be paying $2,911.16 monthly because the house will be twice as expensive.

You want to protect yourself from complete property destruction by carrying home owner insurance. Typical price range is $50 – $100 per month.

Transportation

Despite what you might have heard, it is not practical to live in this US without a car. Public transit systems are not mature enough to get you were you need to be in time that makes sense. If you live in San Francisco and want to go check out a national park – you must drive. If you live in Seattle and bask in the sunlight on Deception Pass – you must drive. Public transit only works in narrow areas around big cities. Besides, you can’t do grocery shopping on a bus. So accept it – you will need a car.

A good resource to research car prices is Kelley Blue Book. You can find cars as low as $3,000 if you are willing to pay cash and do not mind driving a 10 year old car. Typical car prices are around $12,000. Depending on the state and location, you may see people driving $30,000 – $45,000 cars. On the east and west cost, it is not unusual to see $60,000 cars and SUVs.

US national average for a car payment is $460/month. If you go for a $15,000 car and get a typical 5 year loan at a reasonable 3% rate, you’d be paying $270 a month on car alone.

You will have following expenses on top of car payment:

- Car insurance – usually runs about $80 – $100 per month, depending on the driving record.

- Gas – $100 per month for average commuter.

- Maintenance – that’s oil change and small repairs, about $200 a year.

- License tabs – you have to renew car registration annually, which will cost you between $200 – $500 depending on state and car size you are driving.

If you live in a state with a Sales Tax, I’d recommend adding Sales Tax on top of these estimates. So, a well maintained, plain vanilla car will cost approximately $600/month.

Food

Most of the money spent on food will be going on groceries. Median grocery expenses are broken as follows (sources are thestreet.com, usatoday.com):

| Median Annual Income | Average Monthly Groceries |

| $12,000 | $210 |

| $30,000 | $300 |

| $50,000 | $350 |

| $90,000 | $420 |

| $200,000 | $580 |

Table above assumes single individual feeding himself by cooking at home. Of course, this is not practical in social environment, and occasional lunches or nights-out will take place.

- Starbucks cup of coffee – $4

- Sandwitch at Subway – $8

- Cheap restaurant lunch – $20

- Good restaurant dinner – $40 – $60

- Poke plate – $20

- Pho bowl – $15 – $25

- Business cafeteria lunch – $15

- Red robin burger – $15

Health Insurance

This is an extremely important topic for people living in this US. Health care is very expensive and people are required to carry issuance. There are 4 categories of insurance:

- Medical – covers you in case something happens to your body (like a broken arm, head injury, etc.)

- Dental – covers only your teeth.

- Vision – covers your prescription glasses if you need them.

- Prescription – covers any medicine that will be prescribed by doctors.

I will repeat this one more time to make sure it sinks in – every individual in the US is required to have medical insurance by law. If you do not have insurance, you will be penalized by IRS at the time you file taxes. This is no joke, so please get health insurance as soon as possible.

If you work for a reputable company, your employer may sponsor your health insurance and you will be required to pay a portion of premium or nothing at all. There are many carriers and coverage is super complicated so do spend time researching this topic. Largest national carriers are:

Health care insurance can be purchased on Health Exchanges. Available plans, price and coverage will vary wildly depending on your age and pre-existing conditions. On average, however, you can expect to spend $250 – $500 per month on health insurance alone, if you get a deductible of around $6000 a year (which is called High Deductible Health Plan). If you are closer to retirement you can expect to spend $1000 or more per month on health insurance.

Sample medical expenses for a relatively healthy young individual:

- Dentist visit – twice a year cleaning, $200 each visit.

- Eye care – annual exam and prescription glasses – $500

- Family doctor visit – $120

- Over the counter medication – $200 a year

- Emergency room visit – $2,000

- X-ray – $1,500

- Birth of a child at the hospital – $25,000

As you can see, expenses are unpredictable and all over the place.

Utilities and subscriptions

We live in the age where internet is considered a basic human necessity, next to food and whater. You are very likely to need some of these services when you move to the US.

- Internet is available from providers like Comcast, AT&T, CenturyLink, Frontier and a few others – will cost you about $100/month for 100 Mbps connection.

- Cell phone plans from national carries like AT&T, T-Mobile, Verizon will run you anywhere between $50 – $100 a month.

- Electricity may need to be purchased separately, if your landlord does not bundle it up in your rent. It can cost you about $30/month in summer and $60/month in winter.

- Gym membership – 21$/month at LA fitness.

- Amazon Prime – this one is optional and may be unnecessary if you do not plan to purchase from Amazon. If you do – it will run $100 a year.

- Haircut at the barber shop – $15/month. If you’d like to style and color your hair – that’s about $150/month at salon.

- Netflix – approximately $30/month for streaming and DVD mailing services.

- Car wash – washing your car twice a month will set you back $26/month.

- Costco membership – to achieve grocery prices described in this post you’d need about $50 on Costco membership annually.

Lets run the numbers

Now that you have a basic framework, lets put it to work and estimate living expenses of a financially minimalistic 25 year old individual living in Washington state, Seattle, making $100,000 a year and being in great health.

Income before taxes is $100,000. Marginal tax bracket is 24% so adding all taxes from the top of the table till this bracket we get $15,247 in federal taxes. That means, his take home after taxes is $77,104. This guy lives in Washington so no state income tax. We need to calculate his annual expenses to calculate state sales tax.

Housing in Seattle downtown will set him back approximately $2,000/month, which is $24,000/year.

Since our individual is a good driver, his car costs him $230/month, car insurance is $80/month, gas – $100/month, maintenance – $200/year, license tabs in Seattle are expensive, so $300/year. Total car expenses – $5,420/year.

Our individual has a Costco membership – $50/year so his groceries are $500/month. He grabs a coffee on his way to work – $4 x 5 days x 4 weeks = $80/month. He does eat at his company cafeteria – $15 x 5 days x 4 weeks = $300/month. He likes to hang out with his friends on the weekends and spends $100/weekend on food. He is spending $15,410/year on food.

He is healthy so his health insurance is cheap – $300/month. He sees the dentist twice a year – 2 x $200 = $400/year. He catches common cold or needs to boost immune system annually – $200/year. He may need to see a doctor once – $200/year. Our friend’s medical expenses are $4,400/year.

He needs a cellphone and internet – $150/month. To stay healthy he goes to the gym – $21/month. He cuts his hair once every month – $15/month and he binge-watches shows on Netflix – $30/month. He washes the car once every other month – $15/month. Total expenses on subscriptions – $2,772/year.

Overall our individual racked up $52,002 in cost of living expenses. Washington and Seattle combined have 10% sales tax – that’s $5,200.20.

At this point, our individual has $77,104 – $52,002 – $5,200.20 = $19,901.80. With $100,000 annual income, our friend was able to save only a little less than $20,000 for his non-essential expenses like hobbies or travel. That’s less than 1/5th of pre-tax income. And that, my friend, is where the deception lies.