Like most Americans, I indulge in coffee about twice a day. I use the exact same justification as most Americans do – I like the taste of it and it boosts my energy to keep going in this hectic world. It is hard to deny yourself a pleasure of hot tasty cup of awesomeness in the morning. I’d probably amend the constitution to make coffee a fundamental human right (this is a joke).

I track my finances carefully and have noticed that I do not particularly enjoy looking at my spending on coffee. According to a few source like NGPF and TheSimpleDollar, Americans between 25 and 45 spend between $1000 and $2000 a year on coffee, with average spending per day of $3.25. This makes me believe I am not the only one having withdrawal feelings at the end of the credit card billing cycle.

Whole milk tall late at Starbucks costs $3.45 in Washington state with 10% sales tax. I drop by Starbucks after lunch every work day. I began to wonder about financial consequences of cutting my coffee consumption by 1 cup a day.

Invest

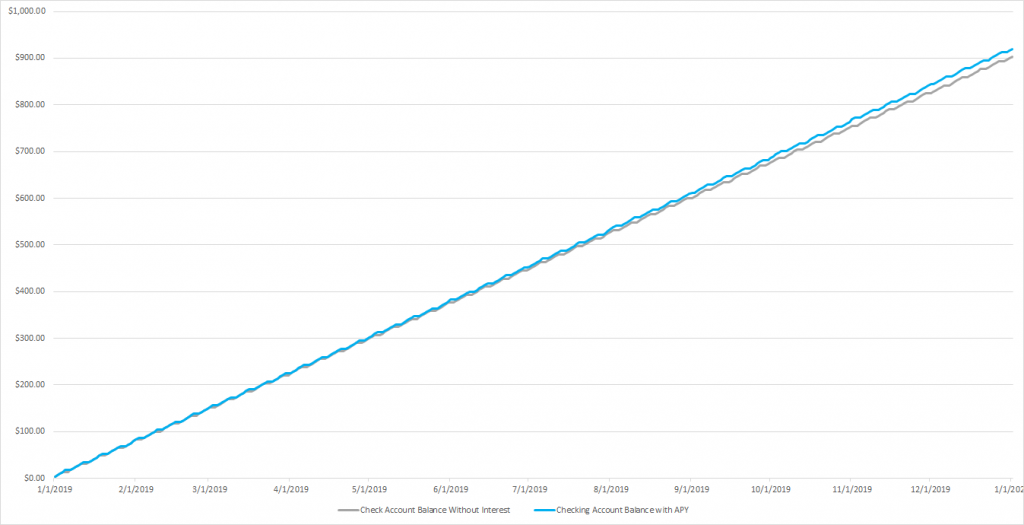

The most obvious way to use this money is to put it into the bank. Most banks and credit unions these days pay some interest on checking accounts. For this calculation, I chose checking account from BECU that pays 4.07% APY on balances up to $500. Savings account pays higher APY but it wouldn’t cut. Federal regulations allow only 6 transactions a month before financial institution is required to charge fees. There are some dinosaur banks that do not pay interest on checking accounts. For completeness, we will do math without interest.

Simple calculation tells us that if we just take the money we would have spent on extra cup of coffee every working day of the year and put into non-interest bearing account, we would be $903.90 rich by the end of the year. Doing the same with interest-bearing account and we’ve got $919.78.

Stock market

Lets try to do better by opening an investment account. Most trading platforms do not charge transaction fees. They allow free transfer and order execution so we are good on this front. Unlike, Robinhood, other trading platforms do not allow partial shares. The smallest amount of shares you can buy is 1, you can’t go 0.34, for example. Let’s stick to traditional platforms, like Fidelity, for our calculations.

I recommend going with proven ETF VOO that has high returns and low expense ratio. This is an index ETF that follows S&P 500 so it has reasonable risk level.

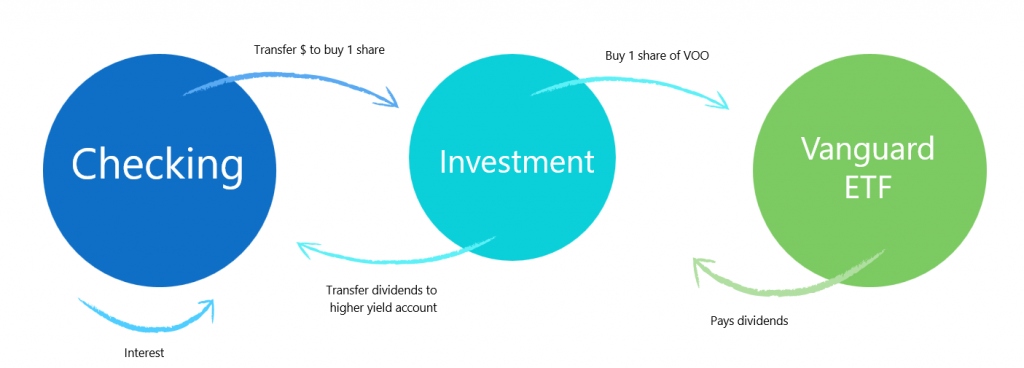

We are going to keep money in the checkin account, shares of VOO in investment:

- Every day we will deposit the price of a cup of coffee into checkin account.

- Money will sit and accrue interest until we have enough to buy 1 share.

- Transfer funds into investment account and buy 1 share of VOO.

- Our ETF will pay us dividends quarterly. We will take that dividend and transfer back into checking account where it yields more interest.

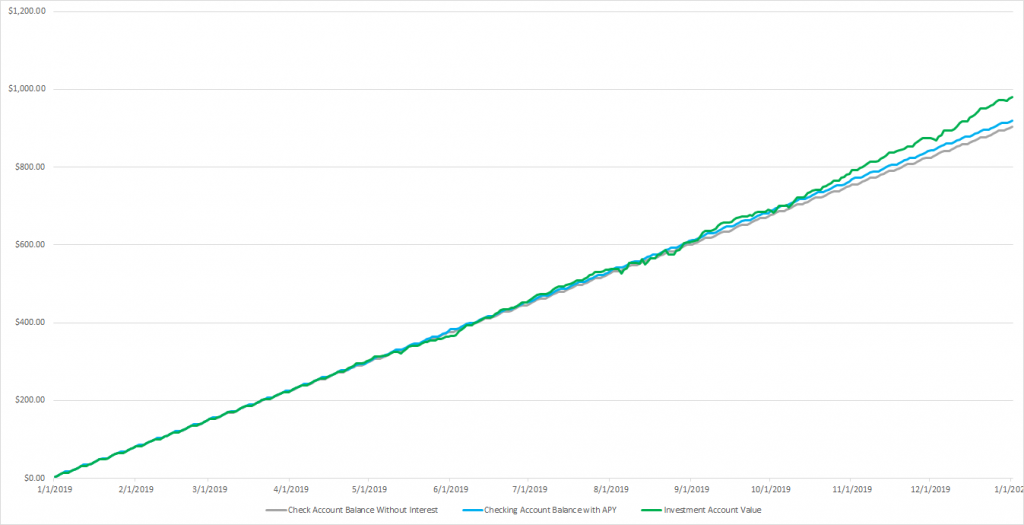

It is pretty apparent that green line representing our investment accounts starts to beat returns from checking account alone. Following this strategy, we were able to amass $980.39 of capital by the end of the year. It is $60.61 more than our previous experiment. We are compounding interest not only on checking account balance but also dividends paid by ETF. In all fairness, biggest factor to growth is ETF equity.

Pay down car loan

Another creative way to use daily coffee savings is to accelerate car loan repayment. According to LandingTree, average new car loan is $32,000. We will use BECU auto loan rates for the calculation below. Average interest is 3.5% for 60 months loan.

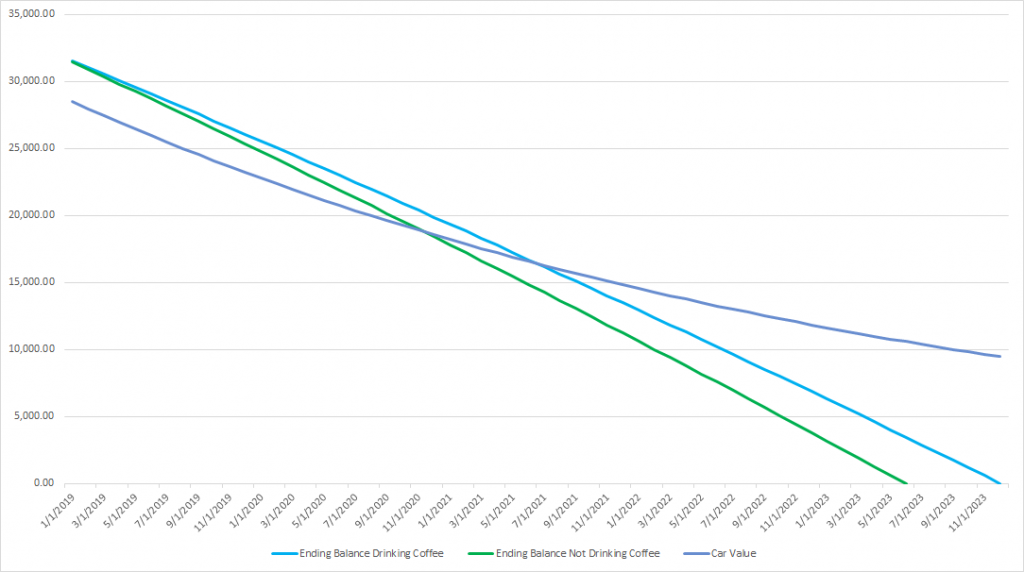

If we pay auto loan as expected without using our coffee money, we’d spend $2,928.12 on interest. Using our coffee money we can add extra $69 per month to principal payment. Chart below demonstrates principal balance over time.

We can see that a small monthly payment reduces our pay-off period by 6 month and brings total interest paid to $2,631.92. This is a net savings of $296.20.

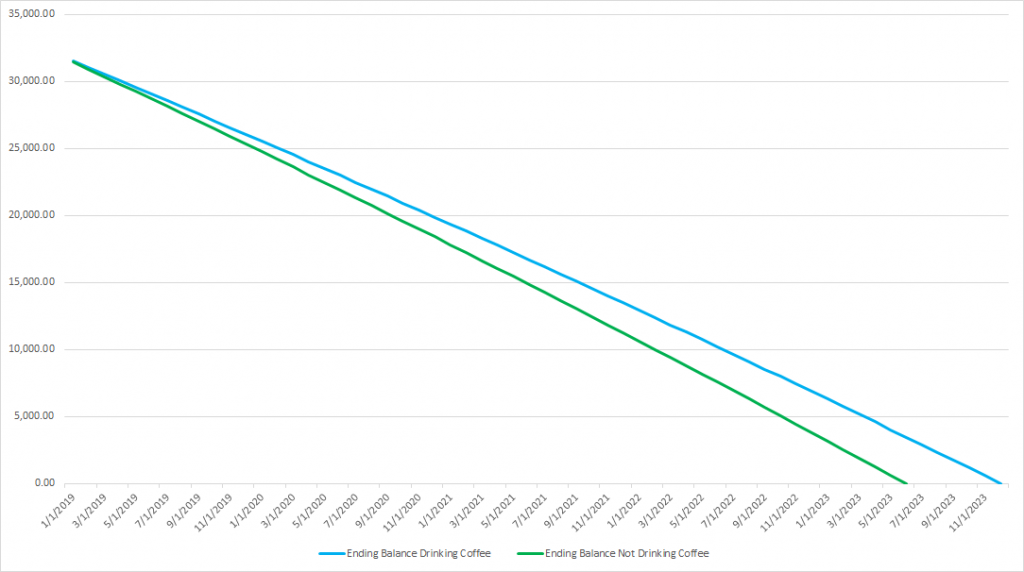

Since this is a financial article, let’s throw car depreciation into the mix to demonstrate the difference of 6 months in repayment period. Car loses value tremendously fast – 11% when you drive it off the lot and 20% year over year.

In case of a traditional loan payment without coffee money (I think I coined the term by now) – $9,463.85. However, if we pay 6 months faster, we be at $10,585.86. This is a difference of $1,122.01 if we were to re-sell the car the moment we pay it off. Adding out interest savings we are looking at $1,418.21 in total savings.

A subtle hint in car value depreciation chart is that financing a depreciating asset with interest is a bad idea.