There are countless videos on YouTube on why real estate is king as well as some videos countering that point of view. Love it or hate it, you can’t deny that US tax code is written to incentivize rental real estate. As a land lord, you can write off almost any expense associated with your property. One very attractive tax write-off is depreciation. When I was just starting, I couldn’t quite figure our exactly which numbers to look at when calculating it. This post should help future investors estimate property depreciation more accurately.

Full disclaimer – I am not a CPA so do not file your taxes exclusively based on this article. Tax code is complicated so you should seek professional assistance to stay safe. The point of this article is to give you ball-park numbers for your potential rental real estate.

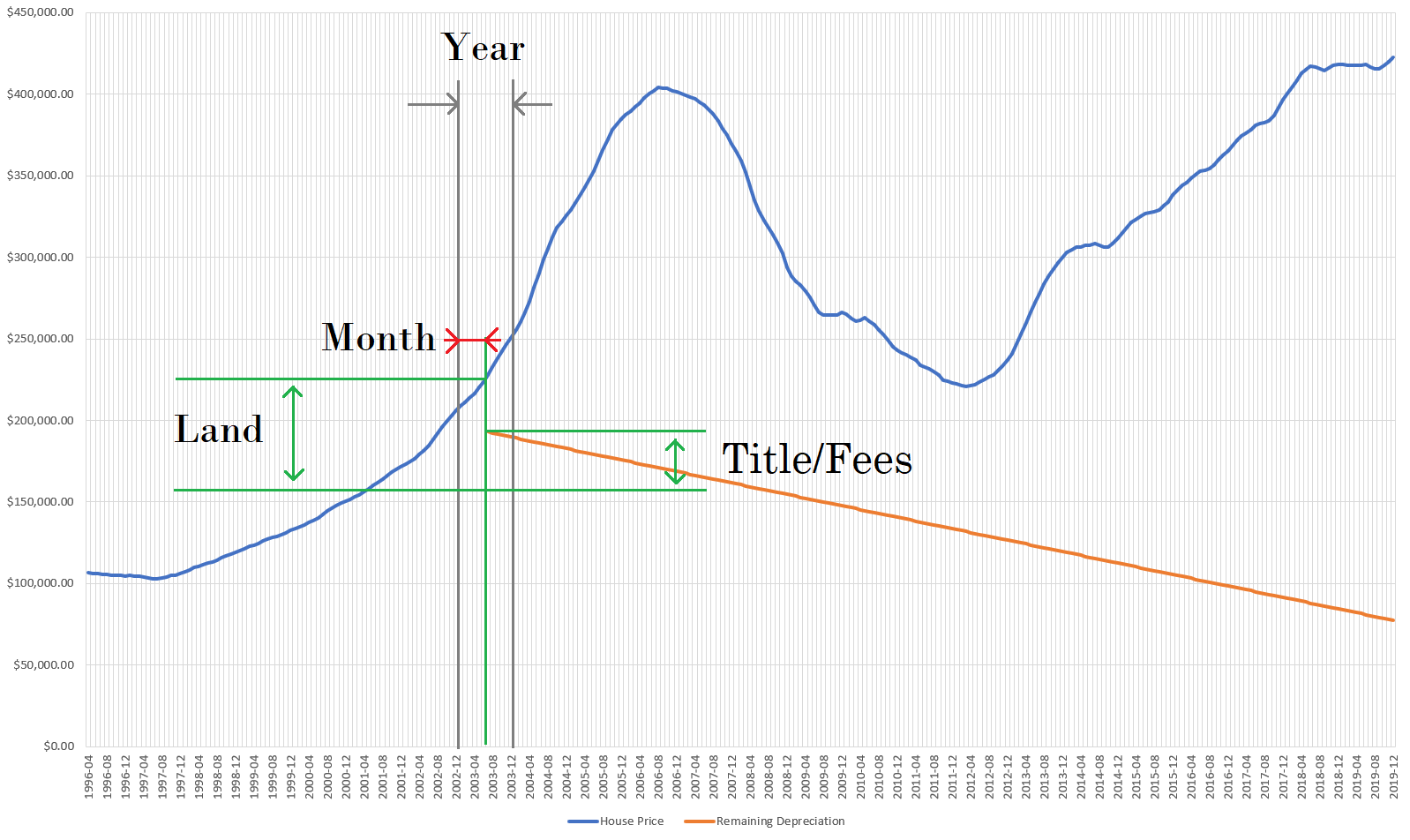

House and Land

The first important input parameter to our formula is the cost of the house itself. Land doesn’t depreciate, but the house built on it does. IRS will accept Property Tax Assessor report or professional commercial appraiser that breaks down the value of the property into building vs land. IRS will not take a swag from Zillow or Redfin. Property prices listed on these websites lump both property itself and the land together because buyers pay for both. However, IRS allows only house to be depreciated.

For the property on our chart, at the time of purchase, combined price was $228,034. Lets say the land portion of it was $50,000. As such, we can depreciate $228,034 – $50,000 = $178,034.

Title and Fees

If you had expenses associated with purchase of the property you can depreciate them as well. You cannot deduct, Sales Tax, unfortunately, except for certain conditions. However, you can depreciate the following items:

- Abstract fees.

- Charges for installing utility services.

- Legal fees.

- Recording fees.

- Surveys.

- Transfer taxes.

- Title insurance.

- Any amounts the seller owes that you agree to pay, such as back taxes or interest, recording or mortgage fees, charges for improvements or repairs, and sales commissions.

You cannot depreciate any of these:

- Fire insurance premiums.

- Rent or other charges relating to occupancy of the property before closing.

- Charges connected with getting or refinancing a loan:

- Points (discount points, loan origination fees).

- Mortgage insurance premiums.

- Loan assumption fees.

- Cost of a credit report.

- Fees for an appraisal required by a lender.

For the property at hand, lets say it costed $15,000 to cover all fees, transfer taxes and get title. As such, our full basis of depreciable property is $178,034 + $15,000 = $193,034. You may be able to depreciate cost of your rental property improvements if you did any. They have to be substantial (for example, paving the front yard) to qualify. Once you factor the cost of all improvements you get adjusted basis of depreciable property.

Depreciation method

Most modern rental properties will fall under Modified Accelerated Cost Recovery System (MACRS) with Straight Line depreciation method over 27.5 years with mid-month convention. Lets break this down:

- IRS will break your depreciable amount by 27.5 years and allows you to claim depreciation for 100% / 27.5 = 3.636% per year of service.

- No matter what day of the month you put property into service, you can only depreciate half of that month.

Interesting aspect to consider is the year when property was put into service. You are unlikely to put the property into service on January 1, it will probably happen a few months after the purchase because you will be making improvements for future tenant. So for the first year, IRS has a dedicated table that spells-out depreciable amount based on the month when property was put into service.

| Month property put into service | Depreciable amount of total adjusted basis |

| January | 3.485% |

| February | 3.182% |

| March | 2.879% |

| April | 2.576% |

| May | 2.273% |

| June | 1.970% |

| July | 1.667% |

| August | 1.346% |

| September | 1.061% |

| October | 0.758% |

| November | 0.455% |

| December | 0.152% |

Looking at our property, we put it into service in July, that means for the first year of 2003 we can depreciate only $193,034 x 1.667% = $3217.87. For all other years, we can depreciate full amount of $193,034 x 3.636% = $7018.71, as long as property stays in service for the full year.

Implications

When you depreciate property, you can’t take advantage of increased property prices. Depreciation starts with the purchase price and doesn’t change afterwards. Even if price of the property at the time of putting it into service is different from purchase price, you still have to stick to purchase price.

When property is sold you must recapture depreciation by filing IRS Form 4797. The gain is assessed against new cost basis after all depreciation is factored in. For example, if property above was sold in 2010 then cost basis of that property would be $193,034 – $3217.87 – (2010 – 2004) x $7018.71 = $147,703.87. However in 2010 this property would cost $243,259 according to market data. As such, we would be paying capital gains on $243,259 – $147,703.87 = $95,555.13, as opposed to $243,259 – $228,034 = $15,225 if we didn’t depreciate it. Exact details of how the tax would be assessed is outside of the scope of this post, I’ll just mention the there will be a portion taxed at recapture rate and the remainder as long term capital gains. However they can be deferred if money is used to buy another property, by filing IRS Form 1033.