In the modern world of a variety of financial products and accounts from different banks, credit unions, investment firms, and others, it is rather hard to make sense of your financial situation without a one-stop-shop solution. To make matters worse, each of your financial products performs differently over time – some years you see great returns and some are barely staying afloat. A centralized view spaning all your cash, stocks, businesses, assets and investments is a prerequisite to financial independence.

If you are just starting your financial life and have 1 or 2 accounts – you should build a habit of tracking your money over time. This will help you live within your means and build wealth. If you are in your thirties and have a plethora of accounts to deal with – you are likely using a tool, and I hope it is not Excel. Financial software is as essential to financial wellbeing as a bat to baseball. In this post, we will cover the advantages and drawbacks of the most popular financial tools out there.

Today we will focus on 3 products that represent different areas of the financial management tool spectrum. If you can last till the end of the article, we will talk about something important that clearly sets one product apart.

Quicken

Quicken is a mature and advanced software that has been on the market since 1983. You need to download it to your PC or Mac to use it. It works well for beginners as well as advanced users, and everyone in between.

This product is not free. You, the consumer, have to pay an annual subscription fee to Quicken to use it. Contrary to popular belief, it costs money to maintain and evolve software – there are designers, developers, operators, management overhead. Everyone needs to eat.

- Quicken supports most, if not all, account types users may have – Checking, Savings, Credit Card, Brokerage, 401(k), 529 Plan, HSA, Morgage, Car Loan, etc.

- It tracks spendings by categories across accounts and can build reports for arbitrary slices – by time, by accounts, etc.

- You can type transactions manually and it will deduplicate them against download transactions.

- You can track paychecks in Quicken, that touch a whole slew of accounts – federal and local taxes, contributions to 401(k), deductions, RSU short sales, etc.

- As an investor, you can use Quicken to track your portfolio performance over time, know when ex-dividend dates are coming up, etc.

- If you happen to be a small real estate investor, you can track your cash flow through Quicken.

- It offers budgeting tools, keeps track of your taxes if you set up a paycheck, and many more things.

Mint

Mint is an online service released around 2006 that caters to masses and offers simplicity. It comes with an iPhone and Android app, but it operates entirely in the data center.

The tool is “free” to consumers, but there is a price to pay. Your financial information is used to advertise financial products to you. This is how they make money. You are presented with “ways to save” and suggestions to reduce expenses by getting a sweeter credit card, car loan or insurance deal. Effectively, advertisers pay for the product.

- Mint gives an easy way to track your Checking and Savings accounts, it neatly categorizes Credit Card spendings automatically.

- It can track your investment portfolio, car loan or mortgage.

- You can set a budget and Mint will let you know if you are deviating from it.

- If you own assets, like a house, you can track them in Mint too.

- Mint can pull your FICO score to let you know where you stand.

GnuCash

GnuCash is a free open-source software that can run on a wide range of operating systems. It targets individuals and businesses that are willing to compromise on features and flexibility but get software for free.

GnuCash is created and maintained by a community of enthusiasts, who likely have day jobs as software developers. Your experience will not be as polished as you get from a commercial product. As such, creators pay for the product and get satisfaction, recognition, and joy in return.

- You can track checking, savings and investment accounts with GnuCash.

- GnuCash has a different approach to categorization than the other tools – it moves transactions into corresponding nested accounts. For example, Expenses\Clothes is an account, rather than a category.

- You can set a budget and track your expenses against it.

- GnuCash is useful for small businesses because you can track vendors, bills, schedule work, and track completion.

- It has a decent set of flexible reports with charts and tables to give insights into your finances.

Feature battle

Not all features are equally important for your financial workflow. Just because a product is jam-packed with stuff, doesn’t mean it is better (like a toaster with built-in GPS). I will list only features that I find valuable.

Not all similar features are identical among products. For example, investment portfolio tracking can be as simple as showing the chart, or as extensive as pivoting all investments by industry across positions in different accounts.

| Features |  Quicken |  Mint |  GnuCash |

|---|---|---|---|

| Ease of use | |||

| Automatic transaction download | |||

| Track future bills and paychecks | |||

| Categorize spendings | |||

| Track net worth over time | |||

| Detailed paycheck breakdown | |||

| Set a budget | |||

| Track investments | |||

| Rich investment tools | |||

| Track asset value over time | |||

| Life time planning | |||

| Rental property cash flow | |||

| Tax due calculation | |||

| Loan and mortgage calculation | |||

| Small business operations | |||

| Customizable reporting | |||

| Integrated bill payment | |||

| Customer support |

Looking at the table above you might think – “this guy is clearly selling Quicken”. I have zero incentive from Quicken to advertise their product. I used all 3 products and I am simply sharing my experience.

Security

Now that we’ve covered financial features let’s talk about something very relevant in the modern world – privacy and security. We hear about companies being hacked left and right. Equifax was hacked and millions of customers’ data exfiltrated. Uber was hacked and 57 million customers’ data was stolen. Facebook data was breached and 50 million accounts were leaked. We will hear about more intrusions and breaches in the future. The battle between hackers and security experts is always in balance. Occasionally, one side or the other prevails, forcing the opposing side to counter-balance and the battle returns to equilibrium. This tug of war will continue for the observable future.

Companies that were compromised have one important trait in common – they all operate on the internet. For them taking their servers offline would be equivalent to going out of business. Facing the two extremes, the industry had to evolve and come up with a set of measures to increase the economic cost of the hack to deter individuals strapped on cash. These measures would not deter state actors, that have substantial resources, but they are effective against shady shops. Here are a few measures I am talking about:

- Zero trust environment – no longer are businesses building perimeter firewalls but rather increasing security on every network flow.

- Authentication and authorization – every individual and a computer on the network must be identified and explicitly granted expiring access to resources.

- Multi-factor authentication – enterprises are excessively employing more than just passwords, but also physical devices or biometrics to confirm user identities.

- Encryption at rest and in transit – at no point data is exposed in free format.

- Data retention governs how long can a business store your data, which should mitigate exposure risk if the company is compromised.

- Threat and vulnerability assessment is continuous run by the companies to catch things that might have been missed in previous points.

As you can see, none of these are guaranteed security barriers, they are best efforts at thwarting attacks. It is still possible to circumvent them if money is not a problem.

Why is this relevant, you might ask? Quicken, Mint, and GnuCash download transactions from your financial institution and store them. How they do it makes a significant difference.

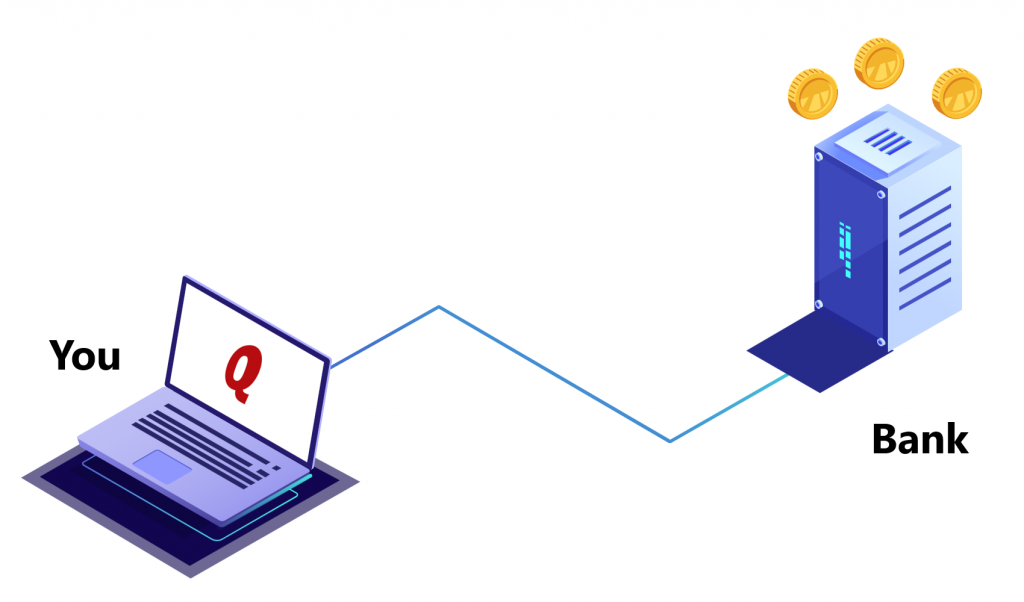

Quicken and GnuCash

Both Quicken and GnuCash have a similar approach to downloading transactions from your bank. They use a method, called “Direct Connect” to connect from your laptop to servers of your bank and pull down transactions. They authenticate using your login and password that you would normally use with your online banking. There is no “man in the middle” – transactions flow directly to your laptop over an encrypted connection.

Once they land on your laptop, Quicken stores them in an encrypted file, protected by a password, unlike GnuCash. So if someone steals your laptop, they won’t be able to access your bank account information without Quicken password, which should be different from all your other passwords used online.

Please note, Quicken does support the “Express Web Connect” method, which sends your login and password to an aggregator service. It is not common for most financial institutions, but some slowpokes still use it. If you are using “Express Web Connect” with your bank – please switch to “Direct Connect” as soon as possible and change your password right away.

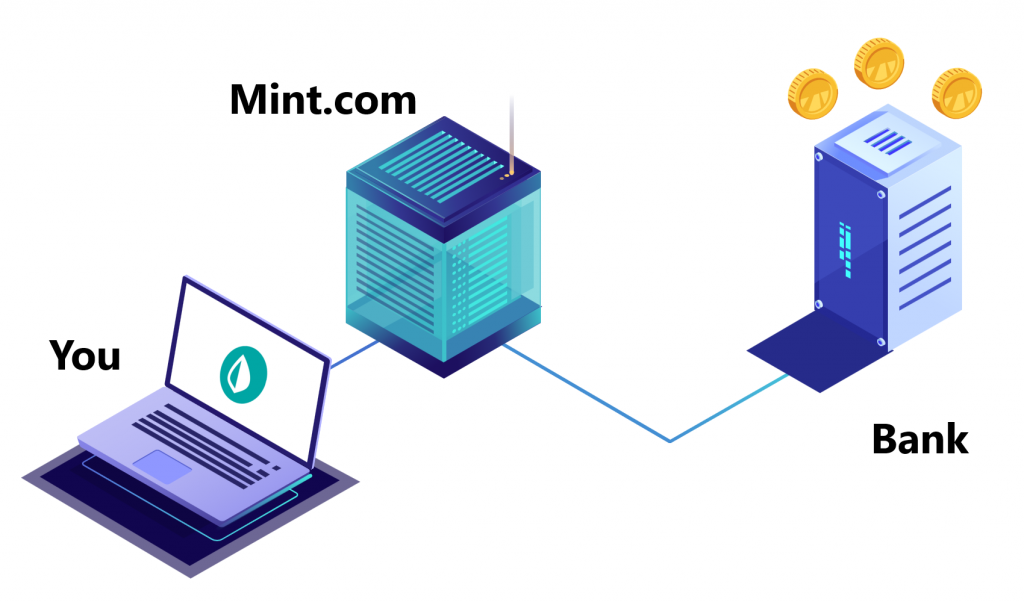

Mint

Mint is a different beast. It is a web service that stores your bank login and password and uses them to download transactions in the background. You log in to the web site with Intuit login and password and Intuit uses your bank’s login and password to show you your transactions.

Mint claims to be a read-only service that can not make changes to your bank. It may even be PCI certified, which I wasn’t able to confirm at the time of writing this article. All of it helps very little because Mint stores your credentials. If Mint is hacked, your logins and passwords can be used to access your bank in non-read-only fashion. Meaning, bad guys can transfer funds, make purchases, do all sorts of damage. Since Mint stores your credentials for multiple banks in the same place, the damage can be quite substantial.

It employs a set of methods that mitigate the risks and reduce the severity of consequences. Mint likely encrypts data it stores, it uses multi-factor auth for its staff when they access your data. I suspect extensive logging and auditing is happening for attribution purposes, should something does south. And if it does go south, they will pay for identity protection services for you for a period of time. Law enforcement will be engaged to catch perpetrators. All of these are mitigating factors. The only prevention to this risk is to not store credentials on their servers, which would render the entire service useless and defeat the purpose of it’s existence.

Conclusion

The state of the personal financial software industry is such that Quicken is light years ahead of everyone else. If you can afford to pay annual subscription fee, this product will serve you well and be secure enough for the peace of mind.

If Quicken is out of reach, I would go for GnuCash before jumping on Mint. GnuCash is not as simple and intuitive as Mint, but it will neither store your credentials on the server nor show you ads to pay for its existence.